What Is Independent Living?

Find independent living near you

Independent living facilities are housing complexes intended for seniors in good overall health. Unlike older individuals who relocate to assisted living facilities, nursing homes, or memory care facilities because they have medical needs, require nursing care, and/or need help with daily activities, moving into an independent living community is more of a lifestyle choice seniors make that offers them supportive services, socializing opportunities, and fewer responsibilities.

Seniors who move to independent living facilities may want to take advantage of freshly prepared meals, amenities such as a community pool or gym, and other benefits such as yard maintenance and housekeeping. Independent living communities range in price, with luxury options often including premium amenities and services. Floor plans vary and may include suites, apartments, condos, and/or cottages.

With all the available options, seniors may wonder, "Where is the best independent senior living near me?" For help locating independent living for seniors, contact Caring.com's Family Advisors at (800) 558-0653. These friendly professionals offer their services free of charge and can help you find a community that provides you with the lifestyle you want that fits within your budget.

Key Takeaways

|

How To Know When It's Time for an Independent Living Facility

Growing older at home may become lonely, isolating, and stressful due to the demanding nature of homeownership. It may even become dangerous if there is no one nearby to rely on in case of emergencies. In contrast, independent living facilities allow seniors to maintain an independent lifestyle while providing community, support, and companionship.

Independent living staff can handle meal preparation and housekeeping, allowing seniors to socialize with other community members, participate in organized activities and outings, and enjoy community amenities.

Is an Independent Living Facility Right for You?

When exploring whether independent living is the right choice for you, consider the following benefits that independent living facilities typically offer their residents.

- Events and outings that promote an active lifestyle and offer socializing opportunities with other seniors

- Opportunities for communal dining, an on-site restaurant or cafe, or a full or partial in-residence kitchen

- Pet ownership

- Housekeeping services, such as the cleaning of living spaces, laundry services, and restocking bathroom supplies and bedroom linens

- Use of on-site gathering spaces for rentals and social events, including dining areas, meeting spaces, libraries, and outdoor areas

- Staff who perform outdoor grounds maintenance such as yard work, snow removal, plumbing, and gutter cleaning

- On-duty staff in case of emergencies who often know CPR and can provide general support

- An age-friendly design intended to accommodate the needs of older adults, with features such as grab bars and wide hallways

Research available services and amenities to help narrow down your options. Keep in mind that no two communities are the same, and if possible, you should visit several providers to determine your ideal fit.

Independent Living vs. Other Types of Senior Care

Understanding the differences between the types of available senior care is crucial. Each option caters to a specific level of needs. Here's how independent senior living compares to other types of senior care.

| Care Type | Shared Spaces + Group Activities | Offers Housekeeping | Help with ADLs* | Offers Skilled Nursing Services | 24/7 Assistance Available |

|---|---|---|---|---|---|

| Independent Living | ✔️ | ✔️ | ✗ | ✗ | ✗ |

| Memory Care | ✔️ | ✔️ | ✔️ | ✔️* | ✔️ |

| In-Home Care | ✗ | ✔️ | ✔️ | ✗ | ✗ |

| 55+ Communities | ✔️ | ✗ | ✗ | ✗ | ✗ |

| Skilled Nursing Facilities | ✔️ | ✔️ | ✔️ | ✔️ | ✔️ |

| Continuing Care Retirement Communities | ✔️ | ✔️ | ✔️ | ✔️ | ✔️ |

| Assisted Living | ✔️ | ✔️ | ✔️ | ✔️* | ✔️ |

*Regular skilled nursing care is sometimes, but not always, offered in assisted living and memory care communities.

Top resources for seniors and caregivers

We have thousands of expert-written articles to help you learn more about care options

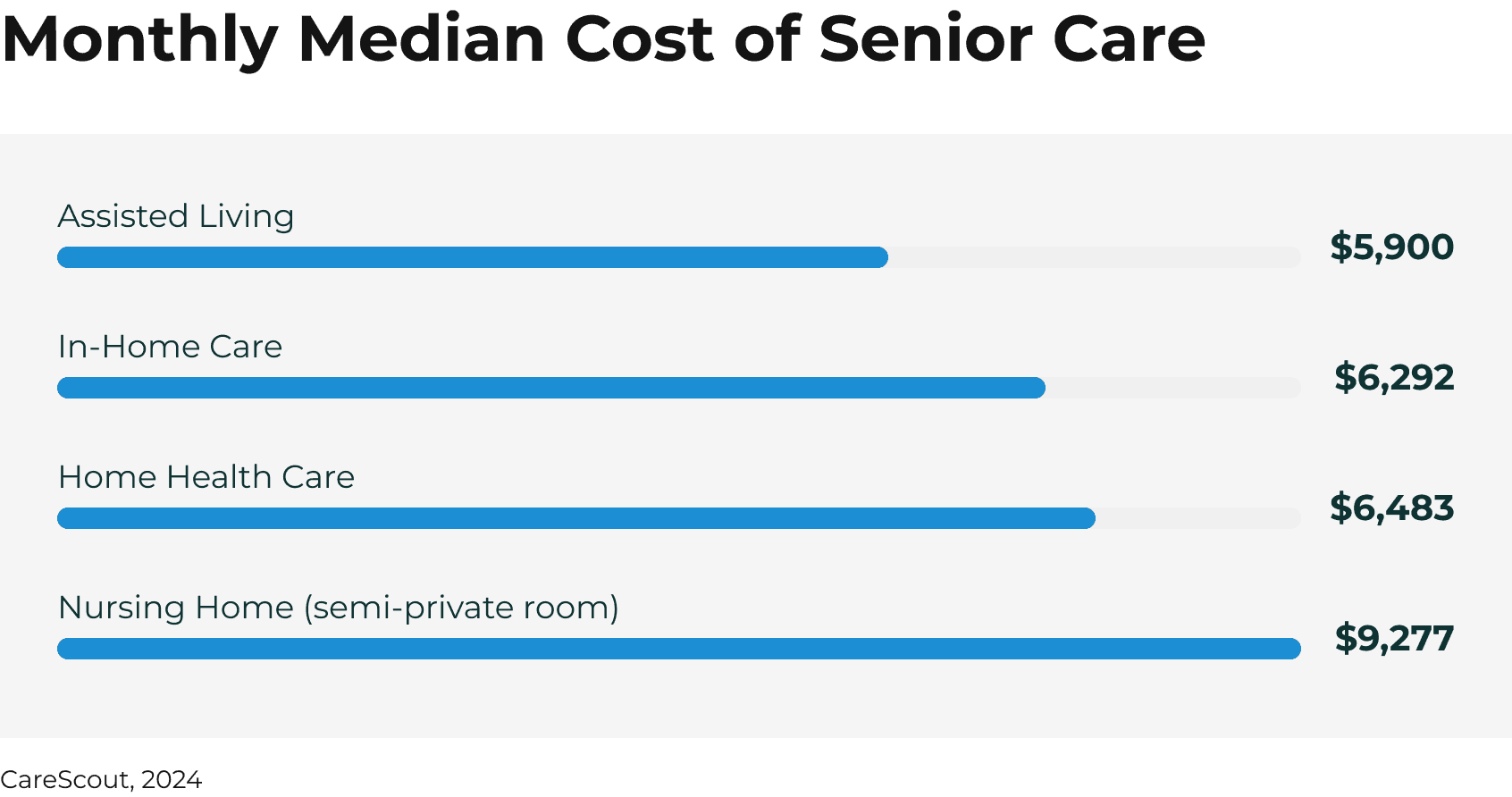

How Much Does Independent Living Cost?

Costs vary based on many factors, including the community's location, the size and type of your accommodations, and the available services and amenities.

Note that rent amounts may increase with time — always check your community's rent adjustment policy before signing any paperwork. Depending on the provider, you may encounter entrance fees and costs for certain meals, activities, and services.

How to Pay for Independent Living

Seniors can look to various resources to cover independent living costs, including life insurance policies, annuities, selling or renting your home, and reverse mortgages. Medicaid or a long-term care insurance policy may also cover some services you may need while residing in an independent living facility.

- Life Insurance: With life insurance, you can borrow against the value of your policy or sell it back to your insurer or a life settlement company to fund your move to an independent senior living community.

- Buy an Annuity: Annuities provide guaranteed regular payments or a lump sum that can go towards the costs of independent senior living.

- Home Sale or Rental: Finance your move to an independent living community by selling or renting out your home.

- Reverse Mortgage: This option lets you pay for assisted living by borrowing against your home's equity.

- Medicaid: This program may cover in-home care services caregivers provide to patients in independent living facilities in certain states.

- Long-Term Care Insurance: Some long-term care insurance policies may cover services received in independent living communities.

How to Find an Independent Living Community?

Caring.com's Family Advisors provide free advice and recommendations to seniors searching for an independent senior living community. Call (800) 558-0653 for assistance from a friendly advisor who can help you select an independent senior living facility that offers your preferred services and amenities.

Independent Living FAQ

Browse our answers hub to find all the answers to your senior care questions.

Top Independent Living Locations

View independent living options in the top-searched locations.

Don’t see your location? Find independent living near you.

Select your state and browse our filterable database to begin

- Alabama

- Alaska

- Arizona

- Arkansas

- California

- Colorado

- Connecticut

- Delaware

- District Of Columbia

- Florida

- Georgia

- Hawaii

- Idaho

- Illinois

- Indiana

- Iowa

- Kansas

- Kentucky

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Minnesota

- Mississippi

- Missouri

- Montana

- Nebraska

- Nevada

- New Hampshire

- New Jersey

- New Mexico

- New York

- North Carolina

- North Dakota

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- Rhode Island

- South Carolina

- South Dakota

- Tennessee

- Texas

- Utah

- Vermont

- Virginia

- Washington

- West Virginia

- Wisconsin

- Wyoming

Find Independent Living in these popular cities

Sources

- Benefits of independent senior living communities. (2024). Seaton Senior Living

- Independent living 101: benefits, types and costs. (n.d.). Westminster

- Casamento, Rich. (2024). What are the benefits of an independent living community? AgingGracefully.com

- What are independent living communities for seniors? (2024). SpringHills.com